A number of news items and events this week have made me think about the world of investment banking again after a few relaxing weeks off for good behaviour.

They have not been happy thoughts.

First of all, there was the announcement of 7,000 layoffs at my old employer Deutsche Bank. It’s a large cull, especially since it will be focused on the investment bank that only employs about 40,000. It was also predictable and predicted. Behind this stark number there are, or will be, 7,000 human stories. A few of my friends and ex-colleagues (talented guys every one, and good, loyal company men, too) have already been shown the exit. It must have been a sad day for them.

On the upside, in recognition of the long term benefits and strategic genius of this move, the market smacked DB stock lower on the day by 4.7%. ‘Every cloud’, as they say.

Now there’s a school of thought that says it should have been 7,001 layoffs. But bank Chairman Herr Achleitner managed to avoid being ousted by (sadly only metaphorically) torch wielding investors at a recent shareholder meeting that was talked of euphemistically as being ‘feisty’.

Given that his tenure in the job could be most charitably described as ‘disastrous’ and more accurately as ‘farcically disastrous’, the 90% support he got surprises me. Maybe the shareholders who made up this 90% are like Kevin Bacon in the film Animal House: all of them assuming the position and shouting ‘Thank you Sir, may I have another?’ after each painful blow with the Fraternity Paddle. Why? I can only imagine it’s as a result of some complex psychosexual issues not related to wealth maximization. I guess we’ll never know.

In the same week as the brutal jobs announcement and the failed peasants’ revolt, the takeover rumour mill started up.

BNP’s CEO was quick to deny that the bank had any intention of buying Deutsche although I suspect that the prospect of a reverse Sedan must have tempted some of the more historically minded and patriotic Board members just a teeny little bit.

On top of that came the strong rumour – first reported by the FT – that Barclays was looking to tie up with Standard Chartered. Both banks have denied this rumour outright and several commentators have poured scorn on the very idea of a merger between these two entities: ‘no fit in strategy or culture’ etc. I have to say that I have seen some widely touted ideas for mergers that are far less plausible than this one though – like BNP with DB or Commerzbank with DB or, indeed, anyone with DB.

But what really caught my eye about the Barclays story was the rumoured motivation for Barclays to consider the deal: namely that it was an attempt by the bank’s Chairman (in contradiction of his CEO’s viewpoint) to “fend off activist investor Ed Bramson, who is seeking to scrap its investment arm.”

So both Deutsche and Barclays are beginning to exit, or are struggling internally against the prospect of exiting, the investment banking arena. For us oldies, this is a massive turnaround, for it was these two banks, back in the early part of this century, which were the great white hopes of creating a European investment banking capability big enough and strong enough to challenge the US’s viselike arm lock on the sector.

They have clearly failed.

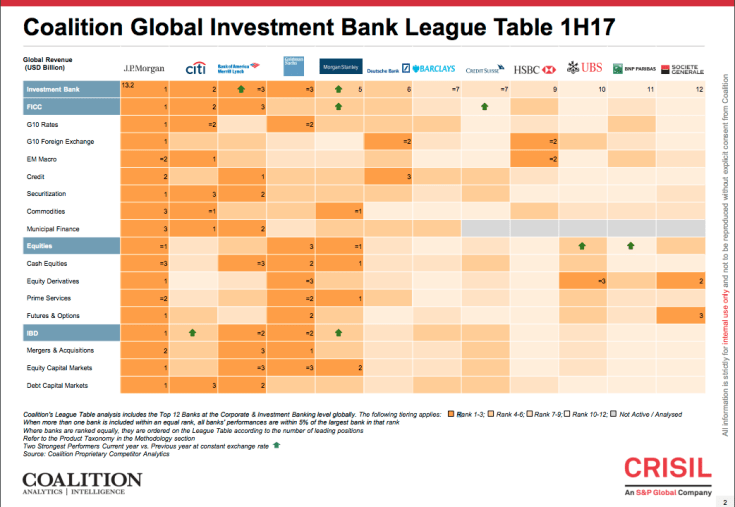

Whether you look at investment banking revenue or market share league tables, the decline of the European challenge is starkly illustrated. Numbers produced by Coalition (a consultancy that specializes in the finance sector and, in my experience in the world of FX, publishes revenue analyses that are bang on the money) show that the top 5 highest ranked firms by investment banking income in the first half of 2017 were all American. There is a link here if you are interested in the details. Or just check out the table.

Leading the pack is the giant J.P. Morgan – in the top three everywhere from M&A to equities to fixed income. Then come Citi, BAML, Goldman and Morgan Stanley – the American bulge bracket. Limping along after them come the Europeans in the following order: DB, Barclays, CS, HSBC, UBS, BNP and SocGen. Bearing in mind that the top two of these banks (DB and Barclays) are now pulling back, the dominance of the Americans looks assured.

What can explain all this?

Just off the top of my head I can list the following reasons that I have heard singly and in combination:

- European regulations are stricter than in the US and thus disproportionally disadvantage the Europeans;

- European firms rely on bank lending not securities so the origination fee pool is smaller;

- The underlying European investment banking market is too fragmented;

- The underlying European retail market is too fragmented (which means lack of efficiencies and thus lack of profit to support investment banking);

- The whole European economy still has not sorted out its debt problems unlike the US;

- Europeans find it harder to penetrate the US markets than the Americans do Europe;

- US regulators have pursued an unfair ‘vendetta of fines’ against the Europeans;

- European culture is not compatible with ‘Anglo-Saxon’ methods employed in investment banking; etc.

I am not sure about the last one – it doesn’t explain Barclays and when I was there Deutsche seemed perfectly happy with the Anglo-Saxon methods of investment banking (when those methods were making most of the firm’s revenues), and – of course – if you can’t find culturally compatible Europeans to run the i-bank, you can always hire some of said Anglo-Saxons. The other reasons probably all have some element of truth.

But one thing that is undeniable – whatever the fundamental cause or causes – is that the scale of European banks is now smaller than that of the Americans. This is vitally important. Parental scale buys you increased reach into a larger customer base for banking deals and for funding. It allows internal cross-subsidies to stabilise businesses that might be in a temporary cyclical downturn (think of FX revenues driven by market volatility, or equity revenues driven by rising stock prices). It allows economies of scale and scope – especially across IT platforms.

Admittedly it also means that the banks can be too big for their management to understand in a crisis, but it appears that this danger isn’t considered a factor right now.

What is startling is how much the scale advantage of the American banks has increased in the last ten years. The next table that I cobbled together shows the market capitalisation of the 12 banks mentioned in the Coalition survey both now and ten years ago. It shows US firms and European firms separately and ranks them by descending market cap.

Only HSBC has a scale approaching the big American firms: every other European bank is smaller than even the smallest US bulge bracket bank. Second placed BAML is slightly bigger than all the Europeans combined (bar HSBC); the disparity between the giant J.P. Morgan and Deutsche is an eyebrow-raising factor of 15.

Back in 2008, however, the top five US banks’ combined market cap of about a half a trillion bucks was lower than the sum of the top seven Europeans. The size ratio of J. P. Morgan to DB was only 2.2:1. Today the US banks are worth about a trillion USD – doubled in ten years – whereas the Europeans are now worth 22% less than what they were. In part this is due to the way that the USD strengthened in those ten years, but market power has clearly shifted dramatically.

And I believe it is the scale disparity that is prompting the current merger chatter. If they really want to compete (and I accept that they may collectively just decide that it’s best to give up) I think the European firms will need to consider consolidating to achieve scale in investment banking. If they don’t they will be shunted aside and will shrink to become peripheral, specialist or merely regional players. This is already happening at Deutsche. If it happens elsewhere, this week’s 7,000 job losses may just be the start.

Then it really will be time to write the obituaries.

Kevin Rodgers’ book ‘Why Aren’t They Shouting?’ is available at Amazon

May 28, 2018 at 11:41 pm

Did you read the interview with David Folkerts-Landau in the Handelsblatt?

http://www.handelsblatt.com/finanzen/banken-versicherungen/david-folkerts-landau-im-interview-chefvolkswirt-der-deutschen-bank-rechnet-mit-der-aera-von-josef-ackermann-ab/22580552.html?ticket=ST-150697-OOkoXwZsaJ5Qd1CvesrP-ap5

Torsten Slok has sent out a translation, it is an interesting hindsight review of DB investment banking expansion over the last 20 years

LikeLike

May 28, 2018 at 11:55 pm

I haven’t Mr. B. But i’ll have a look tomorrow. Cheers.

LikeLike