It’s Christmas and for me that means drinks parties. In the past, knowing that I was meant to be some sort of expert on finance, at least one or two people would ask me about the Euro or UK interest rates or bank stocks or, more usually, internships for their kids.

This year? It’s all been bitcoin: more particularly, bitcoin futures.

First, let me just say upfront that I have no idea what the ‘right’ value for a bitcoin is. Is it $1,000? $10,000? $100,000? Not a clue. And nor has anyone else. Bitcoins are like works of art: they are limited in number and they are worth precisely what people will pay for them. A few months ago that was $1,000; as I write it’s closer to $20,000. That’s rational markets for you.

Second, is the current bitcoin market a bubble? Let me answer that by asking another question: is this an elephant?

It certainly looks like one – it is big, grey and wrinkly and it has tusks and a trunk. Of course, I’m not absolutely 100% sure. It could be a bunch of cats taped together and artfully body-painted grey.

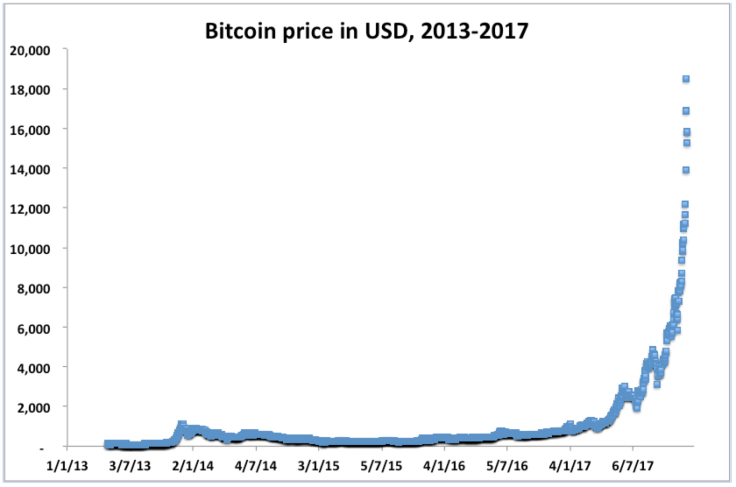

Now here’s the price chart for bitcoin.

If it ain’t a bubble it’ll do until the real bubble gets here.

And it’s this chart’s recent vertiginous rise that is exciting the drinks party chatter. Who isn’t fascinated by a get-rich-quick story? But it’s more than mere interest. Many people I meet feel genuinely unsettled, even hurt by the rise.

In the words of one friend: ‘I hate this sodding bitcoin thing. I haven’t got into it and I feel emotionally short’.

Emotionally short! Were there ever two words any better at explaining history’s weird pops and bubbles in asset prices? The pain and fear of missing out. The miserable sideways glances at the financial pages. The hollow feeling when the news mentions the dotcom / gold / beanie baby / tulip market every damned night – and you’re not in it.

Hence the excitement this week from the serried ranks of unfortunate bitcoin sideline dwellers about the CBOE and CME launching futures on bitcoin. Surely – I’ve heard – this would be the mechanism to halt this pesky trend? Now people can get short bitcoin. There must be someone (please – someone!) who would come in and give this thing a good hard smack and trigger some panicky selling?

So far, a week in, the answer is no they haven’t. Prices are still eye watering and were up about 6% on the Friday (15th December) before I wrote this.

Looking at the CBOE futures closing prices, though, two things are clear.

The first is that volumes are super thin. It’s very early days I suppose and it is coming up to Christmas (a normally fallow time for markets). Even so, only about $27 million worth of the front (January 2018, or F8) future traded on December 15th. [1] The February (G8) and March futures (H8) saw about $3 million each. This is a ‘stock’ that has a market cap measured in hundreds of billions with a daily turnover on a number of exchanges of over $1 billion.

The second thing is that there is a remarkable amount of carry in the futures prices.

For example, with the ‘cash’ bitcoin at $17,680, the January future settled at $18,105 – about 2.4% higher. Put another way – 27% annualized (a/365). The February and March futures are less extreme but still amount to about 9% (and much higher on a ‘last price’ basis)

Finance 101: futures should be priced to avoid arbitrage. But if the price of a future is high relative to the underlying asset there is a classic and simple way to exploit this fact: borrow money to buy the asset and simultaneously sell the future. When you come to settlement, deliver the asset and use the cash to pay back the loan and pocket the excess. Given that bitcoins pay no dividends, you’d be in the money using this strategy if you could borrow money for a month at an annual rate of less than 27%. You could almost a use a credit card.

So why is the carry so high?

The settlement prices could just be flukes in a thin market. It’s possible but the pattern has been there for a few days.

Or maybe the people who are playing around in the futures genuinely can’t borrow for less than 27%? I suppose at a pinch that might be true of the retail market, but there are market making professionals who are involved.

What is probably happening is that retail speculators are buying the futures (I need to get in now and the margin’s only 40 percent!) and professionals are selling. But when the pros sell they need to price in the 27% carry. I suspect the answer to the question ‘why?’ is just that it’s pretty tricky and risky, even as a professional, to put on the arb.

First off, the futures do not physically settle. Rather they are cash settled off the price for bitcoins achieved via an auction on the Gemini exchange. That means to be sure of the arb, you need to own bitcoin at Gemini. It is no easy matter to port bitcoins from other venues: the underlying bitcoin market is extremely fragmented with delays of hours between initiating and concluding a transfer (a very good explanation of why this is the case can be found here). Result? Limited liquidity and widely differing prices by exchange.

And while 27% carry sounds great, actually capturing the spread between cash and the future reliably is a complete pain if liquidity is low and volatility is high. Over half the days in 2017 have seen absolute daily moves in excess of 2.4% (the size of the cash-to-F8 gap) – the volatility of bitcoin is definitely not for the chickenhearted.

These two factors of illiquidity and volatility will not just make ironing out arbitrages difficult: they will make going short – especially in significant size – pretty scary too.

So far then, all in all, the launch of the CBOE bitcoin future – rather than signaling a halt to the bitcoin story – has, instead, merely emphasised the asset’s unique and troubling peculiarities.

It is true that today’s launch of the rival CME future BTC (which unlike the CBOE’s version represents five bitcoins, not one) might work out differently, but I doubt it. For one thing, linking the future to underlying cash for this product is made even more complicated by virtue of the fact that it settles off an index (the Bitcoin Reference Rate or BRR) that combines price feeds from lots of bitcoin exchanges. (I can almost sense the future legal disputes brewing on this one).

The bitcoin bubble will pop one day – the total unsuitability of a rampant and volatile bitcoin for use in everyday commerce and the growing hostility of fiat-currency-issuing governments will likely be the long-term limiting factors – but I don’t think the CBOE or CME contracts will be the cause.

My friend and many like him will have to bear with being emotionally short a little while longer.

Postscript:

One other explanation for why there might be excess carry on the futures prices is that there is concern that if you buy a bitcoin to make up the cash leg of the arb it might not actually be there when you need to hand it over. So-called ‘security risk’. I had thought, given the way blockchain works, that such risk was vanishingly small. But an ex-colleague (more expert than me in this market) pointed out to me yesterday that this is indeed a factor. I therefore post this correction / addendum to my original piece.

My overall conclusion is unchanged however: this is a total bugger of a market to short and the likeliest impediment to its further rise is the threat – or just fear – of coordinated regulation from pissed off governments.

1] Utterly irrelevant I know, but I can’t resist this opportunity to tell you my mnemonic for remembering the futures month codes. Fat Geriatric Hippies Jokingly Killed My New Quails Using Violence eXtremely Zealously. I am truly sorry.

1 Pingback